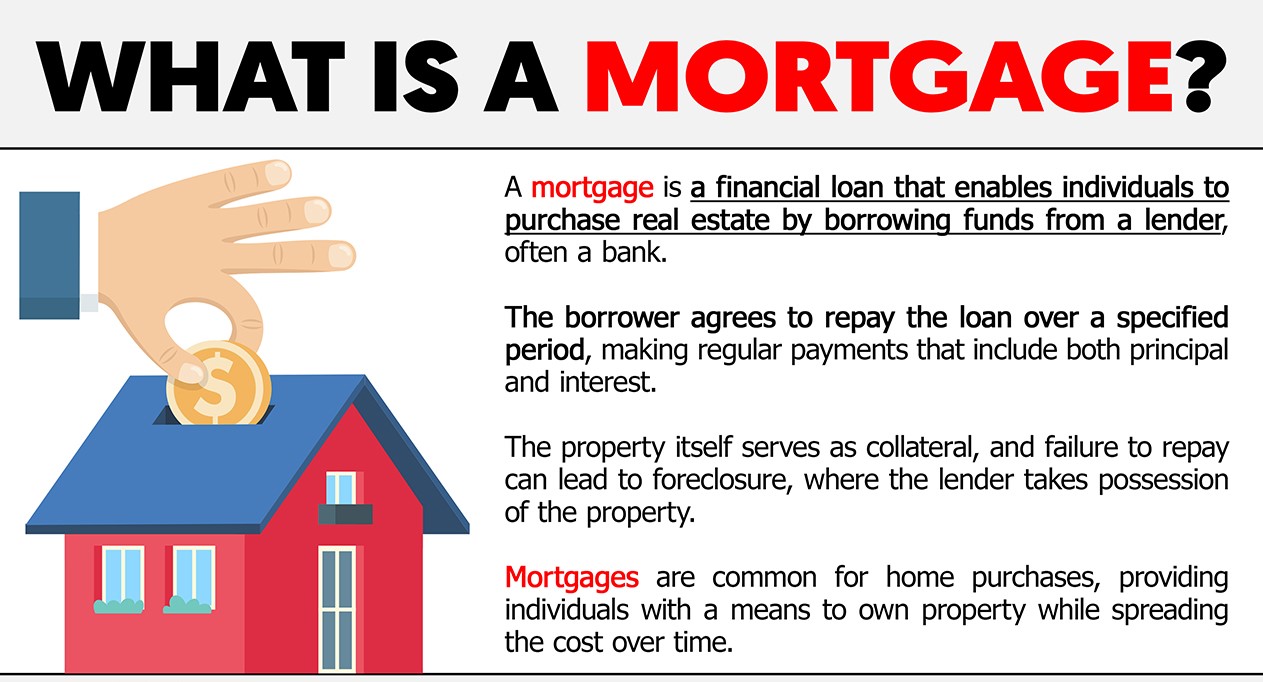

A mortgage is a specific loan to pay for or keep the rights over the property a piece of land, structure, etc. The borrower has to pay the lender back over time, usually in regular payments that include principal and interest. This makes it a secured loan, as the property is security for the entire mortgage. A borrower will be an originator who sells a mortgage” to a potential home buyer across the street, applying for their 5 million dollar loan with whoever they prefer and having them meet at least several eligibility standards, like a minimum credit score.

The home is one of the most significant purchases you will make therefore, financing plays a role in striking any deal. But how does a mortgage work And what are you doing when you build up equity in your home regarding paying down the mortgage. Here is how Mortgages work, basics about mortgages, and a lot more that you should understand to Build Equity in your home.

Mortgages Works

Mortgages are a means by which individuals or businesses can buy real estate without paying the total price in cash upfront. The borrower is granted credit to pay the formal purchase price, which will be repaid over a certain number of years, taking into account equal parts principal and interest payments so that once paid off, they ultimately gain clear property title. Almost all regular home loans are fully amortized.

This means the monthly payment amount will remain consistent throughout, while different amounts get allocated towards principal and interest with each installment. Meanwhile, many mortgages run between 15 and 30 years though a few may have longer terms.

For instance, a homebuyer pledges their house to the lender, and then it becomes called upon by the lender. This guarantees the lender retains an interest in the property if someone does not live up to their financial obligation. If a default occurs, the lender is entitled to take any of those properties, kick out all residents that remain, and sell off each property sold for you to foreclose to pay off your scourge debt.

The Process of Mortgage

It starts with potential borrowers applying to a lender or lenders and being told how much they can afford. The lender will demand proof of financial security from the borrower. Some of those things may be bank and investment statements, your most recent tax returns, or evidence that you are employed. The lender generally checks the credit, too. The lender will preapprove the borrower for a loan of up to an amount with interest.

Pre-approval allows homebuyers to forward a mortgage application after selecting a property to buy or while still shopping for one. A mortgage pre-approval benefits buyers in a competitive housing market and holds their offers, as sellers will know they have the money to provide an offer.

That settlement, or closing, is between the buyer and seller or their proxies. This is the point at which the borrower hands in their deposit to pay for it. For many transactions, and if it is not a cash sale (such as you are getting a conventional loan), then the buyer will need to set up any remaining mortgage documents. At closing, the lender may charge fees to originate the loan usually as points.

Down Payment Financed

You can also borrow less to reduce your mortgage payment (and the interest you pay). Making a down payment is a better way of lowering your borrowing. For example, Say you want a $400k home. As part of the home buying process, you require a down payment of 20%, or $80k.

| Amount borrowed | $400,000 (zero down) | $360,000 (10% down) | $320,000 (20% down) |

| Loan payment | $2,533 | $2,280 | $2,026 |

| Total repayment | $912,425 | $821,002 | $730,280 |

You borrowed less than the full amount because you put down $80,000. Depending on the interest rate, getting a 6.52% loan for thirty years can be a big cost savings overall.

How Does Mortgage Interest Work

Mortgage interest is a huge part of your total cost, so it’s imperative you know how it works. Interest is a penalty and does not pay down your mortgage balance. For most mortgages, a higher portion of each payment goes toward interest.

For instance, that 30-year fixed-rate loan for $360,000 at 6.52% with a monthly P&I of $2,280 per the mortgage calculator, in which you make your first payment P&I payment due on February 2023, etc. The next table shows how it was broken down over time:

| Payment date | Principal | Interest |

| February 2023 | $324 | $1,956 |

| August 2039 | $947.31 | $1,332.69 |

| January 2053 | $2,468.80 | $13.41 |

Mortgage interest is compounded monthly on the remaining principal balance. But your payments are scheduled for so-called amortization. So, amortization paying down the principal balance. In other words, during that initial month, for the most part, you are paying interest on a loan of $2280 with only $324 going to pay down your principal.

Your principal balance next month would be $359,676 ($360,000 – $324). That next $2,280 payment will pay a little bit more toward the principal, but you’ll pay just slightly less on interest. As time passes, more and more loan amortization is applied towards the principal, with your last monthly payment being almost entirely interest.

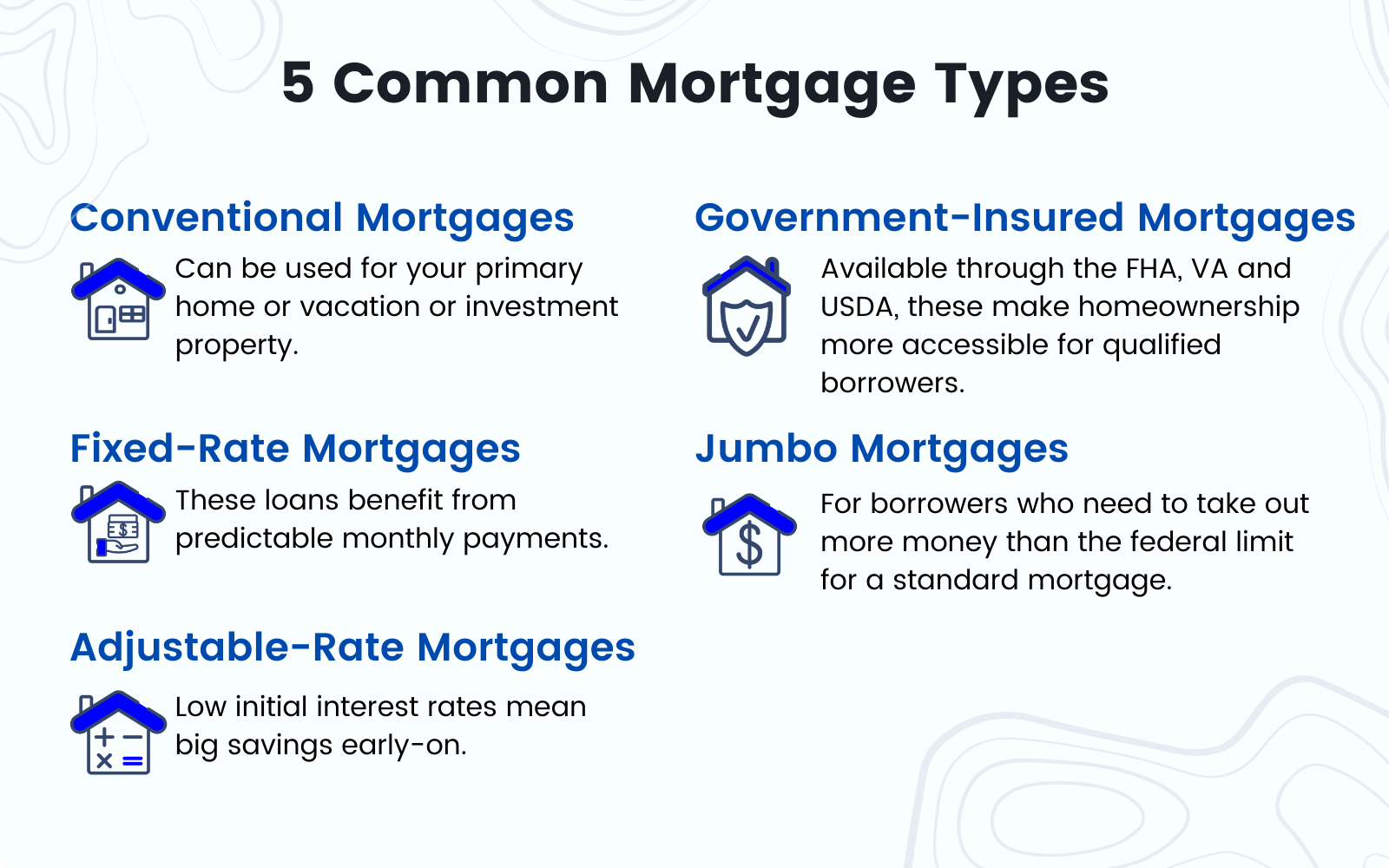

Types of Mortgages

The most common mortgage products are 30-year and 15-year fixed-rate mortgages. For this reason, mortgage terms can be as short as five years and go up to 40 or more. A longer repayment term lessens your monthly payment but increases the total interest cost over a loan’s life. Within the same year down-payment range as in the 2010 lineup Versus today when most government-backed types offer no money upfront, which exploded due primarily to local housing.

Choice while still requiring higher levels than ever before income limits on those two groups have soared with-upshots overall substantial growth of loan volume through FHA vs USDA plus separation between borrowing options based upon where they stand financially further growing apart . Below are a few of the mortgage loan types offered to customers.

Fixed-Rate Mortgages

Most loans are structured as fixed-rate mortgages. A set-rate home loan means the passion upon your monthly payment is additionally compensated in that interest—the much more common fixed-rate mortgage.

Consider an Adjustable-Rate Mortgage

An ARM is a home loan with an interest rate periodically adjusted based on changes in a specified market index. The teaser rate is usually lower than market rates, making it more affordable upfront but less so over time if you experience a significant spike when your mortgage resets. ARMs or adjustable-rate mortgages are developing a bad reputation.

Interest-Only Loans:

Lastly, fewer types of mortgages, such as interest-only and payment-option ARMs, have repayment terms that can be difficult for less sophisticated borrowers to understand. This usually means the loans are coming due with a big balloon payment. As these types of mortgages reset, many homeowners. It ended up in financial ruin during the early 2000s housing bubble.

Reverse Mortgages

Reverse mortgages aren’t as different as they sound. These loans are specifically for homeowners 62 and over, allowing them to take a portion of their equity in the home as cash.

The homeowners can draw value out of the home whether in one big rollover or monthly payments that continue as long as they live there. The loan balance becomes due when the borrower dies, ceases to live in a home, or sells it.

Average Mortgage Rates

How much you will pay for a mortgage is determined by the type e.g., fixed vs. adjustable, term 10 or 30 years, optional discount points paid at closing, and interest rates prevailing when the fees are settled. Futures -Interest rates can change from one week to the next and between lenders, so it makes some sense to do your shopping.

Throughout 2020 and 2021, mortgage rates fell to historic lows, marking their lowest point in nearly five decades. Between the beginning of the pandemic (about April 2020) and Jan. 2022, that average was below just over 3.50% on a very popular benchmark—or as low as a record nadir of only 2.65%. 345.

However, in 2022 and 2023, mortgage rates increased to higher historical records than ever before. Neither the 30-year fixed-rate average nor its sub-components have surpassed an over-7% threshold since Sept. Before that; it last hit more than two decades ago in Oct. 1992 with interbank readings up to a high at least very close to a, if not topping out right, then-eye-watering annual rate peak equal or greater than this year’s pinnacle:

- 30-year fixed-rate mortgage: 6.77

- 15-year fixed-rate mortgage: 6.05%

How to Compare Mortgages

Until recently, banks and savings and loan associations thrifts or S&Ls were just about the only outlets for mortgages. But Better, which is not a bank lender, offers you the ability to do so today. Com, along with Loan Depot and Rocket Mortgage, continue to hog a growing piece of the mortgage market.

Mortgage shoppers and those hoping to move into a new home can use online calculators, which are the quickest way of getting an idea of what your monthly mortgage payments might be based on different interest rates or annual interest, types of mortgages, and amount you want to borrow no matter if it is fed by high or low down payment.

Alongside the loan principal and interest, your lender or mortgage servicer may set up an escrow account to cover local property taxes, homeowners’ insurance premiums, and other costs. You should only have S20,000 or so extra, which will eat away at your mortgage every month.

Also, keep in mind if you make less than a 20% down payment on your home loan, the lender may require that you pay private mortgage insurance (PMI) which will be paid for each month.

FAQs:

Why Do People Need Mortgages?

For most families, the cost of a home trumps whatever savings they have. That’s why we have Mortgages to assist individuals or families in buying a house by paying the lender (or seller) an upfront payment, typically 20% of the purchase price, so that what they borrow is enough to buy the house. Then, it is followed by the property in the market if his aural will not pay.

Can Anybody Get a Mortgage?

This may change with the new arrangement, under which all prospective borrowers must apply through mortgage lenders for approval from an underwriting process. They will only issue home loans if these factors are met so that those with a house and an asset and income ratio can pay off the cost of doing so over time.

A mortgage will also be factored in based on a person’s credit score. The mortgage interest rate is also bucketed, resulting in those closer to defaulting suffering an extra layer of risk.

In any case, you can own or mortgage one or a combination of them through an agreement.

Home loans are often handled through banks and credit unions, as are many mortgage outfits that strictly do home loans. You may also shop for rates with various lenders through an independent mortgage broker.

Can You Have More Than One Mortgage on Your Home?

Additionally, lenders generally prefer when the first mortgage is in place before agreeing to a second. This is known as a home equity loan or, more loosely, the second mortgage. Even less common is a junior loan secured by the home you have an FHA or VA first mortgage on.

The bottom line is that you can take out as many junior loans on your home as you have equity for, and the DTI supports them (plus whatever pairs with your credit score).

Why Is It Called a Mortgage?

The word comes from Old French and Old English mort death gage- pledge or vow. Hence, things are running with some loans from the hell of a title when this sort of claim is paid off and when the borrower has defaulted.

2 thoughts on “What is Mortgage, How They Works and Types”